Looking at 2025 as a whole, it is clear that the leather and leather goods, textile, raw material and end-consumer product segments have gone through a multi-layered transition period. Evaluating the sector primarily through end-consumer demand and pricing behaviour helps us better understand the bigger picture.

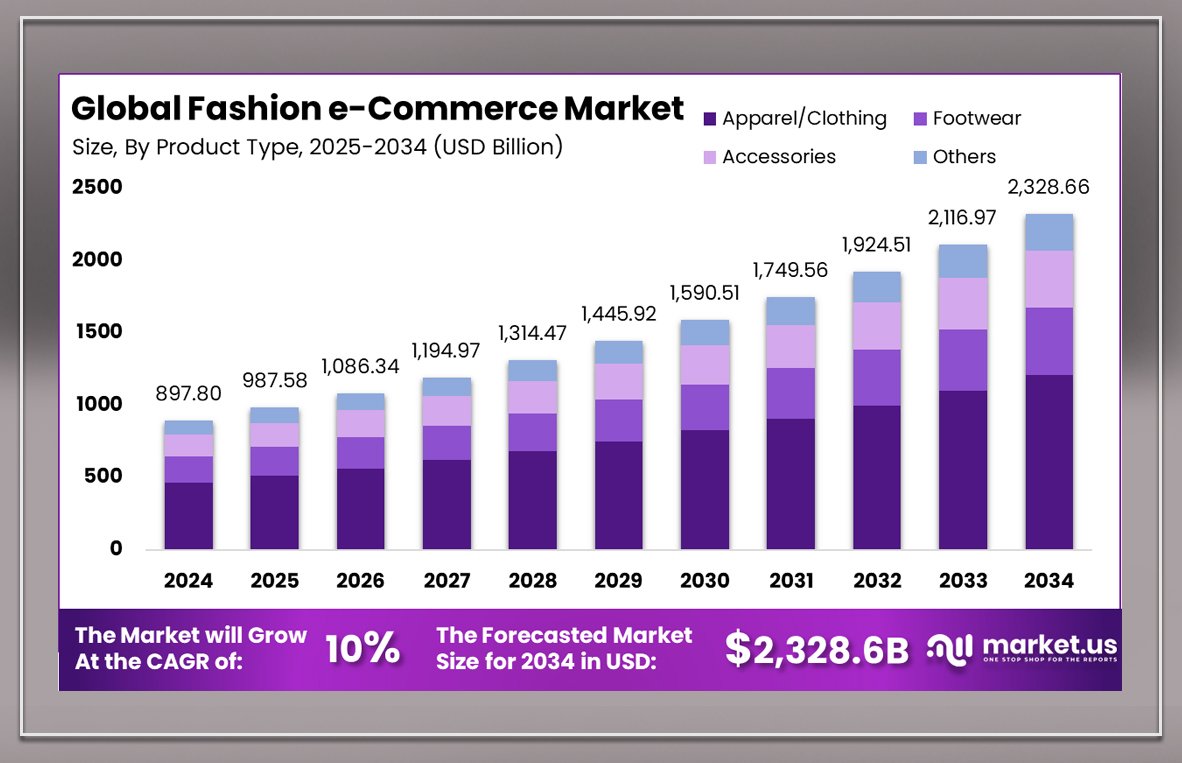

One of the most striking indicators of 2025 has been the average 30% growth in digital sales channels. Brand-owned websites, online marketplaces, Google-based shopping tools and AI-powered recommendation systems have played a decisive role in this growth. Based on national retail and e-commerce statistics, this figure represents a global average trend, despite regional differences.

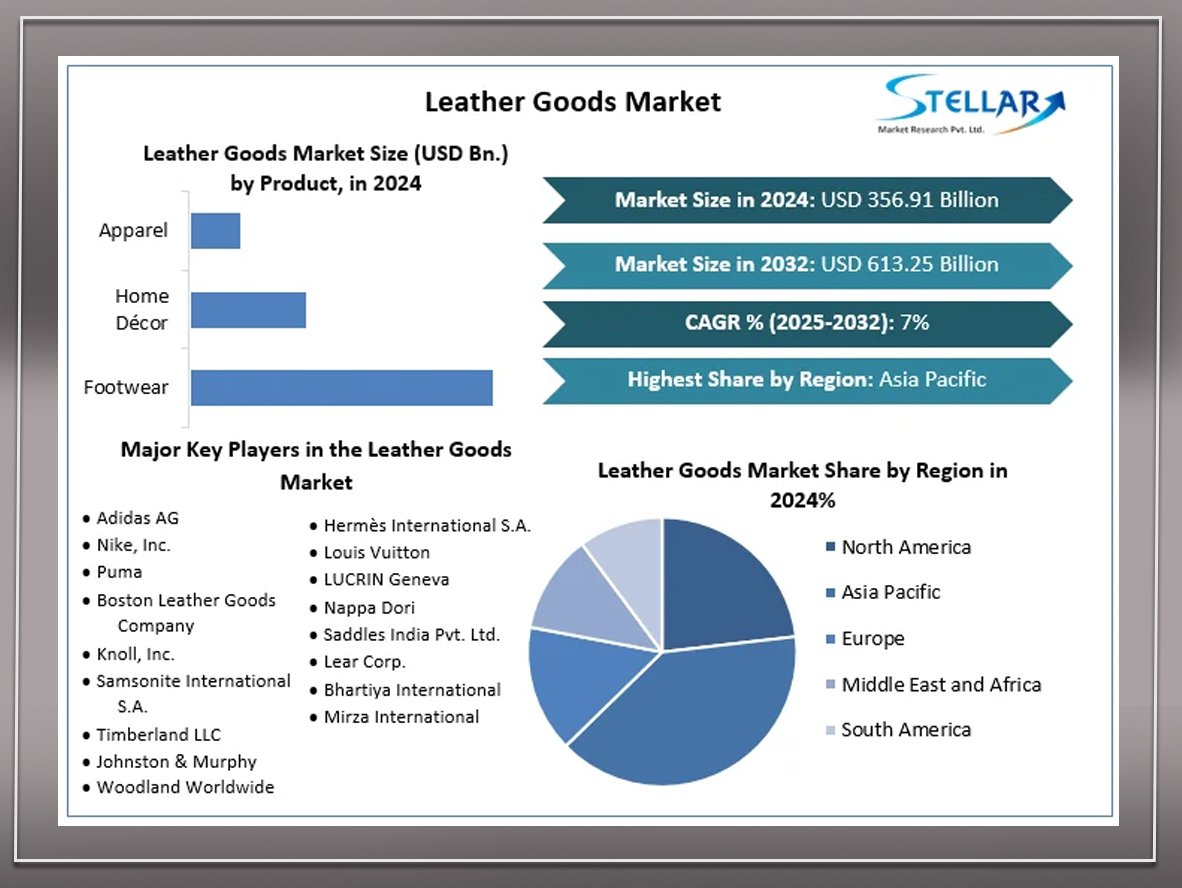

In terms of product categories, consumers primarily purchased bags, belts and wallets in leather and synthetic materials, while trousers and T-shirts led textile sales volumes. A key observation is that most sales were concentrated in the mid-price segment, rather than premium price ranges. High-priced products remained limited, while accessible price points dominated market activity in 2025.

Leather products, however, present a more balanced picture. End consumers appear more willing to accept reasonable price levels for genuine leather products. Yet a critical challenge remains: many consumers struggle to clearly distinguish between genuine leather and synthetic (vinyl/faux leather) materials. This highlights the growing need for clearer product information, material transparency and consumer education.

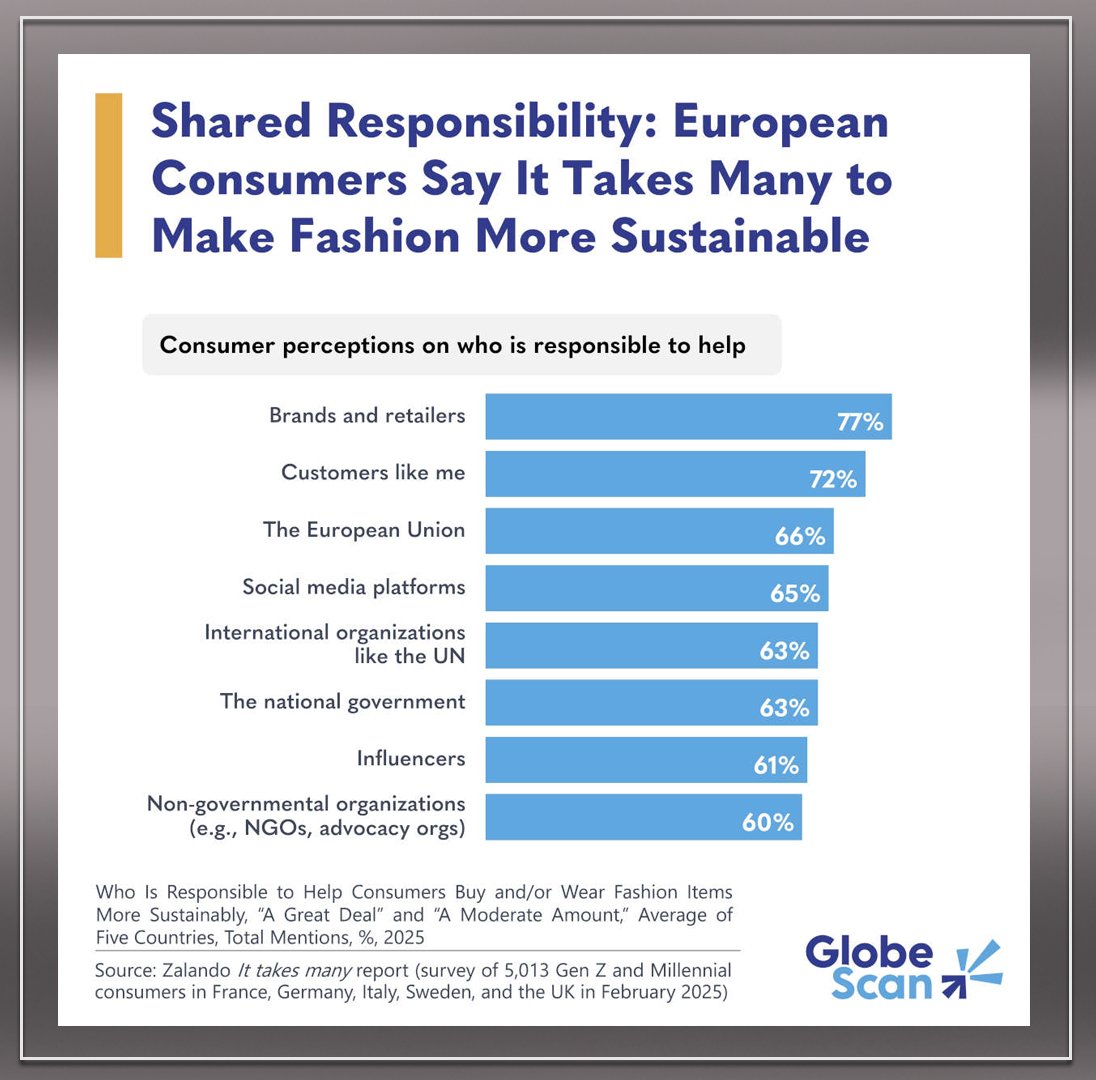

Sustainability has also moved beyond marketing language. Consumers actively look for sustainability claims — but increasingly question whether a product is truly sustainable. As a result, traceability, production transparency and material disclosure on labels have become essential. Tools such as QR codes, digital product passports and transparent supply chain communication have proven to be trust-building elements throughout 2025.

On the production side, 2025 was a challenging year due to economic fluctuations. Export data across multiple countries indicate figures slightly below historical averages. Ongoing geopolitical conflicts have restricted trade routes and export opportunities, directly affecting consumer purchasing priorities. Unsurprisingly, luxury segments were among the most impacted.

This context highlights a critical need: building a strong bridge between producers and end consumers. Informing consumers about how a product is made, under which conditions and why it is priced as it is, supports not only sustainability but also efficient sales and long-term brand loyalty. This approach is relevant across all market segments, not only luxury.

As we enter 2026, economic instability is likely to persist. However, one reality is clear: the future of the sector does not lie in producing more, but in using resources efficiently and delivering environmentally responsible, traceable products. This is no longer solely an industry issue — it is a shared responsibility for all of us as end consumers.

With the hope that 2026 will transform the lessons of 2025 into balanced strategies, improved efficiency and renewed stability — and with the sincere wish for peace, restored purchasing power and global economic recovery.

See you in the next column.

{kind=link}